Best car loan rates and financing companies are key to getting the best deal. Navigating the maze of loan options can feel overwhelming, but this guide breaks down everything you need to know to find the perfect financing for your dream ride. From understanding different loan types to identifying top providers and assessing loan terms, we’ll equip you with the knowledge to secure the lowest possible interest rate and make the most informed decision.

We’ll explore the factors influencing interest rates, delve into the application process, and provide strategies for obtaining the best rates. Beyond traditional financing, we’ll also examine alternatives like leasing and private loans, and discuss recent market trends and developments. This comprehensive guide will equip you with the tools to secure the ideal car loan and avoid costly mistakes.

Introduction to Car Loan Rates and Financing

Navigating the world of car loans can feel like trying to decipher a cryptic code. But fear not, car enthusiasts! Understanding car loan rates and financing options is key to securing the best deal and getting behind the wheel of your dream ride. This guide breaks down the complexities, highlighting the factors that influence interest rates and outlining the different types of loans available.

Car loan rates are influenced by a multitude of factors, impacting your monthly payments and overall cost of the vehicle. Essentially, these rates are a reflection of the risk the lender takes on by financing your purchase. Factors like your credit score, the loan term, and the type of vehicle all play a role in determining the interest rate you’ll be offered.

Car Loan Interest Rates: Key Influencing Factors

Interest rates are determined by a complex interplay of economic conditions, lender policies, and your individual financial profile. Lenders assess the risk of loan defaults based on creditworthiness and loan terms. A higher credit score generally translates to a lower interest rate, as it indicates a lower risk of default. Loan terms also significantly impact rates; longer terms typically result in lower monthly payments but higher overall interest paid. The type of vehicle, whether new or used, also affects interest rates. Used car loans often carry higher interest rates due to the increased risk of depreciation and potential mechanical issues.

Types of Car Loans

There are various types of car loans catering to different needs and situations. Understanding these distinctions is crucial to making an informed decision.

- New Car Loans: These loans are typically offered for brand-new vehicles and often come with competitive interest rates, thanks to the vehicle’s lower depreciation risk. New car loans often have shorter terms, and the lender often has a better idea of the car’s true value.

- Used Car Loans: Used car loans cover pre-owned vehicles. Since used vehicles are subject to depreciation and potential mechanical issues, interest rates tend to be higher than for new car loans. Lenders typically scrutinize the vehicle’s history and condition before approving a used car loan.

- Subprime Car Loans: These loans are for borrowers with less-than-perfect credit scores. They often carry higher interest rates compared to loans for borrowers with excellent credit, reflecting the higher risk for the lender.

- Dealer Financing: Often offered through the dealership, dealer financing can be a convenient option. However, interest rates might not be as competitive as rates you can find from other lenders.

Loan Type Comparison Table

This table provides a concise overview of different loan types, highlighting key features.

| Loan Type | Loan Term (Years) | Typical Interest Rate (Example) | Eligibility Criteria |

|---|---|---|---|

| New Car Loan | 3-7 | 4-8% | Good credit score, proof of income |

| Used Car Loan | 3-7 | 6-10% | Good to fair credit score, proof of income, vehicle inspection |

| Subprime Car Loan | 3-7 | 10-15% | Lower credit score, proof of income, potentially higher down payment |

| Dealer Financing | 3-7 | 5-9% | Variable, often requires dealership’s approval |

Identifying Top Financing Companies

Source: 1apo.com

Navigating the car loan market can feel like trying to find a needle in a haystack. With so many lenders vying for your business, how do you choose the best one for your needs? This section dives into the world of car loan providers, comparing and contrasting their offerings to help you make an informed decision.

Finding the right car loan provider is crucial. Different companies cater to varying needs and budgets. Some prioritize low interest rates, while others excel in quick approvals. Understanding these nuances is key to finding a lender that aligns with your financial goals.

Leading Car Loan Providers

A variety of companies dominate the car loan landscape. Major players often have established reputations, vast networks, and extensive experience in financing vehicles. This allows them to offer a wide range of products and services, from traditional loans to specialized financing options. Factors like customer service and online accessibility also play a significant role in a company’s overall appeal.

Competitive Interest Rates

Interest rates are a major determinant in the cost of borrowing. Companies with consistently competitive rates attract a large customer base. These rates are often influenced by factors like the borrower’s credit score, the loan term, and the current economic climate. Keeping an eye on these rates allows you to make a more informed choice, potentially saving you thousands of dollars over the life of the loan.

Reputation and Customer Reviews

A company’s reputation speaks volumes about its reliability and commitment to customer satisfaction. Customer reviews, both positive and negative, offer valuable insights into the borrower experience. Looking at reviews across various platforms can provide a more comprehensive view of the company’s service. A strong reputation, backed by positive reviews, can offer confidence and peace of mind during the loan process.

Key Features and Benefits of Top Financing Companies

| Company | Interest Rate Range (Example) | Loan Term Options | Customer Service Rating (Example) | Key Benefits |

|---|---|---|---|---|

| Company A | 4.5% – 7.5% | 24 – 84 months | 4.5 out of 5 stars | Fast online application process, excellent customer support, wide range of loan options. |

| Company B | 5.0% – 8.0% | 36 – 72 months | 4.2 out of 5 stars | Strong focus on first-time car buyers, competitive rates, streamlined paperwork. |

| Company C | 4.8% – 7.0% | 36 – 60 months | 4.7 out of 5 stars | Exceptional customer service, flexible repayment options, competitive interest rates for high credit scores. |

This table provides a snapshot of some key aspects of major financing companies. It’s important to remember that individual experiences and outcomes can vary. Always research specific terms and conditions to ensure a loan aligns with your needs.

Understanding Loan Application Process

Navigating the car loan application process can feel daunting, but it doesn’t have to be a mystery. This comprehensive guide breaks down the steps involved, from initial inquiry to final approval, equipping you with the knowledge to confidently pursue your dream car.

The application process for a car loan typically involves several key steps, each designed to assess your financial capacity and creditworthiness. Understanding these steps will streamline the process and significantly increase your chances of getting approved for a loan with favorable terms.

Application Initiation

Initiating the application process usually involves a preliminary inquiry. This initial step allows you to explore various loan options and understand the specific terms offered by different financing companies. Contacting multiple lenders and comparing interest rates, loan amounts, and repayment terms is crucial. Thorough research and careful consideration will help you make informed decisions.

Document Gathering

A crucial aspect of the application process is the collection of necessary documents. These documents serve as proof of your identity, income, and credit history. Failure to provide the required documents could significantly delay or even prevent loan approval.

- Identification Documents: Valid government-issued photo identification, such as a driver’s license or passport. These documents verify your identity and legal standing.

- Proof of Income: Pay stubs, tax returns, or other official income statements for the last few months, demonstrating your consistent income stream.

- Proof of Residence: Utility bills, bank statements, or lease agreements, validating your current address and residential stability.

- Credit Report: A copy of your credit report, reflecting your credit history and financial responsibility. A strong credit score is often a prerequisite for favorable loan terms. Lenders use this information to evaluate your risk profile.

- Down Payment Details (if applicable): Documentation of the down payment amount and source. This might include bank statements or proof of savings.

Loan Approval Process, Best car loan rates and financing companies

The loan approval process is a multifaceted evaluation of your financial standing. Lenders thoroughly scrutinize your credit history, income verification, and other submitted documents to assess your ability to repay the loan.

- Credit Check: Lenders conduct a thorough credit check to evaluate your creditworthiness and assess your payment history. A good credit score is typically associated with a lower interest rate and quicker approval.

- Income Verification: Lenders verify your income to ensure your capacity to meet the loan’s repayment obligations. Consistency in income is a significant factor in the approval process.

- Loan Application Evaluation: The lender assesses your application based on the submitted documents and your credit history. They analyze your overall financial profile to determine the loan’s feasibility.

- Loan Offer: If your application meets the lender’s requirements, they issue a formal loan offer, outlining the loan terms, interest rate, repayment schedule, and other pertinent details.

- Loan Acceptance and Closing: Upon accepting the loan offer, you sign the necessary documents, and the lender finalizes the loan. This marks the completion of the loan process.

Application Flowchart

Assessing Loan Terms and Conditions: Best Car Loan Rates And Financing Companies

So, you’ve found some car loan options, but now what? Navigating the fine print of those loan terms can feel like deciphering ancient hieroglyphics. Don’t worry, we’re breaking it down, making sure you’re not just signing a contract, but understanding the terms.

Loan terms are more than just numbers; they’re the bedrock of your car financing agreement. Understanding them is crucial to making an informed decision, avoiding hidden costs, and ensuring you’re getting the best possible deal.

Loan Amount and Its Significance

The loan amount is the total sum you’re borrowing. It’s directly tied to the price of the car and any potential down payment you’re making. A larger loan amount often means higher monthly payments, but it could also potentially open the door to more attractive interest rates, depending on the lender. Think of it like this: a bigger house requires a larger mortgage.

Interest Rate: The Price of Borrowing

The interest rate is the cost of borrowing money. It’s expressed as a percentage and determines how much extra you’ll pay over the life of the loan. Higher interest rates lead to higher total payments. For example, a 5% interest rate on a $20,000 loan will cost you more than a 3% rate. Lenders consider various factors when setting interest rates, including your credit score, the loan amount, and the prevailing market conditions.

Repayment Period: How Long Will You Pay?

The repayment period dictates how long you’ll be making monthly payments. A shorter repayment period usually means higher monthly payments but lower total interest paid. Conversely, a longer repayment period leads to lower monthly payments but more interest paid overall. Consider your budget and financial goals when choosing a repayment period.

Loan Fees and Charges: The Hidden Costs

Loan fees and charges are often buried in the fine print, but they can significantly impact your overall cost. These fees can include origination fees, prepayment penalties, late payment fees, and more. Understanding these fees upfront is critical. They can add up quickly, so don’t just glance over them!

Examples of Different Loan Terms and Associated Costs

Let’s look at a few examples:

- Loan A: $20,000 loan amount, 4% interest rate, 60-month repayment period, origination fee of $200. This results in a monthly payment of approximately $380. The total interest paid will be roughly $1,600.

- Loan B: $20,000 loan amount, 6% interest rate, 72-month repayment period, no origination fees. This leads to a monthly payment of approximately $300, but the total interest paid will be roughly $2,400.

Key Points to Compare Loan Offers

When comparing different loan offers, focus on these key points:

- Total cost of the loan: This includes not only the interest but also any fees.

- Monthly payment: This should fit comfortably within your budget.

- Loan terms and conditions: Carefully review the entire loan agreement to understand all aspects.

- Customer service and support: A reputable lender will provide exceptional customer service and support.

Comparison Table of Loan Terms and Conditions

This table summarizes key loan terms and conditions for easier comparison:

| Loan Offer | Loan Amount | Interest Rate | Repayment Period | Fees | Monthly Payment | Total Interest |

|---|---|---|---|---|---|---|

| Loan A | $20,000 | 4% | 60 months | $200 | $380 | $1,600 |

| Loan B | $20,000 | 6% | 72 months | $0 | $300 | $2,400 |

| Loan C | $25,000 | 5% | 60 months | $300 | $480 | $2,000 |

Strategies for Obtaining the Best Rates

Source: keepasking.com

Snagging the best car loan rates and financing options can feel like a wild goose chase, but finding the right deal is totally doable. Think about how crucial steady shots are for capturing awesome moments, and check out Adjustable tripods for taking stable photos and videos for some serious tripod inspiration. Ultimately, securing the perfect car loan is all about comparing rates and finding a financing company that works for you.

Don’t get caught in a price trap—research, compare, and drive off into the sunset with a sweet new ride!

Unlocking the best car loan rates isn’t just about luck; it’s a strategic process. Understanding the factors that influence your interest rate, and actively working to improve them, is key to getting the lowest possible financing. This involves more than just browsing websites; it’s about proactively managing your financial profile.

Knowing your financial situation and how it impacts your loan application is critical. Factors like your credit score, debt-to-income ratio, and even your down payment amount all play a part in determining the interest rate you’ll receive. Being proactive and understanding these elements is the first step towards securing a favorable car loan.

Building a Strong Credit History

A strong credit history is paramount for favorable car loan rates. Lenders assess your creditworthiness to gauge your repayment capacity. Consistent on-time payments on existing debts, like credit cards and loans, demonstrate responsible financial habits. This history of timely payments significantly impacts your credit score, which in turn directly affects the interest rate you’re offered. A higher credit score often translates to lower interest rates.

Credit Scores and Car Loan Rates

Credit scores are a numerical representation of your creditworthiness, calculated based on your payment history, amounts owed, length of credit history, new credit, and credit mix. A higher score typically indicates a lower risk to lenders, leading to more favorable interest rates. Lenders use credit scores to assess your ability to repay the loan. For example, a credit score of 700 or higher usually qualifies for lower interest rates compared to a score below 660. Understanding how your credit score impacts loan rates is crucial for making informed decisions.

Negotiating Loan Terms

Negotiation is a powerful tool in securing the best possible car loan terms. Don’t hesitate to discuss your financial situation with the lender. Communicating your needs and circumstances can often lead to favorable modifications. Knowing the current market rates, and comparing them with the rates being offered, helps you negotiate effectively.

Tips for Securing the Best Loan Rates

- Check your credit report regularly: Identify any inaccuracies and address them promptly. A clean credit report is a strong starting point for securing a favorable loan.

- Improve your credit score: Pay your bills on time, maintain a low credit utilization ratio, and consider paying down existing debts.

- Shop around for loan offers: Compare interest rates and terms from multiple lenders to identify the best possible deal.

- Consider a larger down payment: A larger down payment reduces the loan amount, potentially leading to a lower interest rate.

- Negotiate the loan terms: Don’t hesitate to discuss the interest rate and other terms with the lender. Be prepared to walk away if the terms aren’t favorable.

- Maintain a low debt-to-income ratio: A lower debt-to-income ratio demonstrates your ability to handle the loan payments, making you a less risky borrower.

- Consider a co-signer: A co-signer with a strong credit history can enhance your chances of securing a loan with favorable terms.

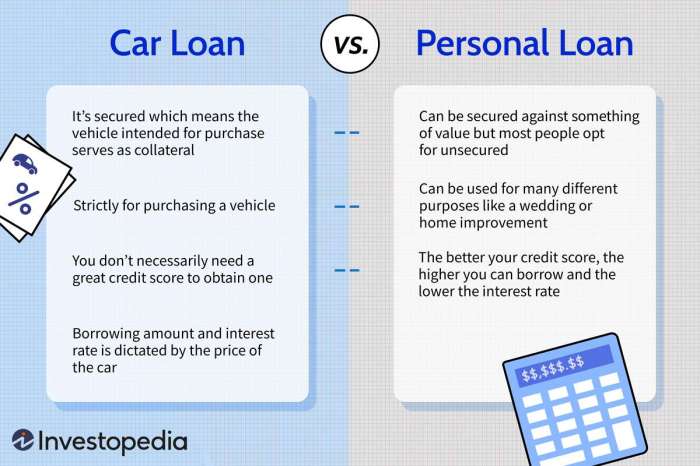

Alternatives to Traditional Financing

So, you’ve got your heart set on that dream car, but traditional car loans feel a bit…blah? Fear not, fellow car enthusiasts! There are other avenues to explore for securing your ride. Let’s dive into some exciting alternatives to traditional financing.

Alternative financing options can be a smart choice, offering different terms and conditions that might better suit your individual financial situation. Understanding the pros and cons of each method will help you make an informed decision about which path best aligns with your goals.

Leasing

Leasing allows you to use a car without owning it. You pay a monthly fee for the use of the vehicle, and at the end of the lease term, you can return the car or purchase it. This is a great option for those who value flexibility and want to avoid the burden of car ownership expenses, like repairs and maintenance.

- Pros: Lower monthly payments, often reduced maintenance responsibilities, and the possibility of upgrading to a newer model at the end of the lease term.

- Cons: You don’t own the car, potentially higher total cost over time compared to buying, and you’re limited to the lease terms.

Leasing is a great option if you’re someone who values a newer model but isn’t necessarily set on keeping the car for a long time. For example, a young professional who anticipates changing cars frequently might benefit from leasing.

Private Loans

Private loans are borrowed from individuals or companies outside of traditional financial institutions. These loans can sometimes offer competitive interest rates and flexible terms, but they often come with more stringent requirements for approval and can be more challenging to obtain.

- Pros: Potentially lower interest rates than traditional loans, more flexibility in terms and conditions, and can sometimes be quicker to process.

- Cons: Higher risk of rejection, potentially more complex paperwork, and may have higher interest rates compared to traditional loans depending on the lender.

Consider private loans if you have a strong credit history or are seeking a loan with unique terms, such as a shorter repayment period. This option could be more attractive to someone who wants to avoid the typical loan application process.

Comparison Table: Traditional Financing vs. Alternatives

| Feature | Traditional Financing | Leasing | Private Loans |

|---|---|---|---|

| Ownership | Own the vehicle | Don’t own the vehicle | Potentially own the vehicle, depends on terms |

| Monthly Payments | Usually higher initially | Often lower initially | Can vary, sometimes lower |

| Total Cost | Potentially higher over time due to ownership costs | Potentially higher total cost due to potential purchase at the end | Can be lower or higher than traditional loans, depending on terms and interest rates |

| Flexibility | Less flexible terms | Flexible; can upgrade vehicles | Potentially more flexible |

| Requirements | Credit check and income verification | Similar to traditional financing | Can be more stringent, often involves a personal guarantee |

Choosing the right financing method depends heavily on your financial situation and goals. Carefully weigh the pros and cons of each option to find the one that best fits your needs.

Recent Trends and Developments in Car Loan Financing

The car loan market is constantly evolving, influenced by a multitude of factors. Understanding these trends is crucial for both borrowers and lenders to make informed decisions. Interest rates, economic conditions, and even regulatory changes can significantly impact the availability and cost of car financing.

Recent Trends in Car Loan Rates and Market Conditions

Interest rates for car loans have fluctuated significantly in recent years, often mirroring broader economic trends. Periods of high inflation, for instance, typically correlate with higher borrowing costs. This dynamic makes it vital to stay updated on current market conditions. Furthermore, competition among lenders has increased, leading to more diverse loan options and potentially better rates for borrowers. This competitive landscape encourages lenders to adapt to changing market demands and customer preferences.

Future Projections for Car Loan Financing

Forecasting future car loan financing trends involves considering multiple variables. Experts anticipate that interest rates will likely remain somewhat volatile, responding to fluctuations in economic growth and inflation. Additionally, the increasing adoption of digital lending platforms may streamline the loan application process and lead to more competitive rates for consumers. Technological advancements will likely continue to reshape the industry, influencing the way loans are processed and administered. For example, the rise of online car dealerships and online loan applications has already begun impacting the financing landscape.

Regulatory Changes Impacting the Car Loan Market

Government regulations play a significant role in shaping the car loan market. Changes in lending regulations can impact the availability of credit, loan terms, and even the overall cost of borrowing. Lenders must adapt to these evolving rules and guidelines, and borrowers should be aware of how these changes may affect their ability to secure financing. For example, new regulations on lending practices for high-risk borrowers can influence the availability of loans for those consumers.

Impact of Economic Factors on Car Loan Rates

Economic factors are crucial drivers of car loan rates. Strong economic growth, often accompanied by low unemployment, usually translates to lower interest rates as lenders feel more confident in the borrower’s ability to repay. Conversely, economic downturns, characterized by high unemployment and inflation, typically lead to higher interest rates. For instance, during the 2008 financial crisis, car loan rates surged as lenders became more cautious about lending. This exemplifies the direct relationship between economic conditions and car loan financing.

Key Takeaways from Current Trends

Several key takeaways emerge from the current trends in car loan financing. Interest rates are likely to remain volatile, responding to broader economic conditions. Digital lending platforms are reshaping the application process, potentially leading to more competitive rates. Regulatory changes will continue to influence the market, impacting both lenders and borrowers. Finally, understanding the impact of economic factors on loan rates is vital for both lenders and borrowers to make informed financial decisions.

Resources and Further Information

Source: optimole.com

Navigating the world of car loans can feel like a maze. Thankfully, there are plenty of resources available to help you find your way to the best financing deal. From online tools to expert advice, this section provides a compass for your car loan journey.

Knowing where to turn for help is crucial. Whether you’re a seasoned car buyer or a first-timer, these resources will empower you to make informed decisions. Armed with the right information, you can avoid costly mistakes and secure the best possible car loan terms.

Reliable Websites and Resources

Finding reliable information on car loan rates and financing is essential for making sound decisions. Numerous websites offer comprehensive resources. Sites like the Consumer Financial Protection Bureau (CFPB) and the Federal Trade Commission (FTC) are excellent starting points, offering detailed explanations and consumer tips on car financing. These sites often feature updated information on current market trends and potential scams to be aware of. Checking the websites of major credit bureaus, such as Experian, Equifax, and TransUnion, is also important to understand credit reports and scores. These resources can help you understand your current financial standing and how it might affect your loan application.

Reputable Consumer Protection Organizations

Consumer protection organizations play a vital role in safeguarding your interests when dealing with financial institutions. These organizations provide a valuable avenue for redress if you encounter problems with your car loan. The CFPB, mentioned earlier, is a crucial resource for resolving disputes and filing complaints. Other organizations, such as the Better Business Bureau (BBB), offer complaint platforms and resources for evaluating the reliability of financial institutions. The National Association of Consumer Advocates (NACA) also provides support for consumer rights.

Filing Complaints About Financing Issues

If you encounter problems with your car loan, knowing how to file a complaint is essential. Each financial institution and consumer protection agency has a specific process for handling complaints. Start by documenting the issue thoroughly, including dates, amounts, and any correspondence. Review the lender’s terms and conditions and any relevant loan documents. Next, contact the lender directly to attempt a resolution. If you’re unsuccessful, reach out to the appropriate consumer protection agency. The CFPB, as mentioned before, is a valuable resource for filing complaints and seeking guidance. They often have a clear process for reporting concerns, ensuring you get the support you need.

Understanding Credit Scores and Credit Reports

Your credit score significantly influences the interest rate you’ll receive on your car loan. Understanding how credit scores are calculated and how to improve them is crucial. Credit bureaus like Experian, Equifax, and TransUnion provide detailed information on credit reports. These reports contain a summary of your credit history, including payment history, outstanding debts, and credit utilization. By understanding your credit report, you can identify areas for improvement and take steps to boost your score. Many websites and financial institutions offer resources and tools for monitoring and improving your credit.

External Resources

- Consumer Financial Protection Bureau (CFPB): This agency is a critical resource for consumer protection in financial matters. They provide information on consumer rights, complaint procedures, and resources for resolving disputes. Contact information: Visit their website at [www.consumerfinance.gov].

- Federal Trade Commission (FTC): The FTC is another important resource for consumer protection, offering information on fraud prevention and consumer rights. Contact information: Visit their website at [www.ftc.gov].

- Better Business Bureau (BBB): The BBB is a non-profit organization that evaluates businesses and provides a platform for resolving consumer complaints. Contact information: Visit their website at [www.bbb.org].

- Experian, Equifax, TransUnion: These credit bureaus provide comprehensive information about your credit reports and scores. Contact information: Visit their respective websites.

This comprehensive list of resources provides a solid foundation for navigating the complexities of car loan financing. By utilizing these tools and information, you’ll be well-equipped to make informed decisions and secure the best possible terms for your car loan.

Summary

In conclusion, securing the best car loan rates involves a careful analysis of various financing options. Understanding the nuances of different loan types, comparing reputable financing companies, and meticulously evaluating loan terms are crucial steps. By considering alternative financing options and staying updated on market trends, you can maximize your chances of getting the most favorable car loan. Ultimately, this comprehensive guide empowers you to make an informed decision, securing the best possible financing for your car purchase.